Bussiness

Dell’s AI Server Business Now Bigger Than VMware Used To Be

We have been watching the big original equipment manufactures like a hawk to see how they are generating revenues and income from GPU-accelerated system sales. These OEMs provide the best indicator of the health of the GenAI revolution and the efforts to democratize the massively parallel – and massively expensive – type of computing AI training and inference systems require.

Up until now, companies like Dell have not really had much of a play when it comes to GenAI because of the shortages of GPU accelerators, mostly from Nvidia. Those shortages were not just caused by the complexity of manufacturing a modern GPU platform, but also by the hoggy behavior of the hyperscalers and cloud builders – along with more than a few national HPC centers. But in the long run, revenues and profits at Dell and its OEM peers will depend on normal companies across all industries and geographies paying the normal OEM premium for AI servers as well as for general purpose machines with CPUs.

In its latest financial report, which is for the quarter ended on August 4 and which is the second quarter of fiscal 2025, Dell is beginning to show some signs of commercializing GenAI, starting with the Tier 2 service providers and clouds and large enterprises that have a case of Nvidia NvyTM real bad now.

Sales of AI servers are certainly starting to affect the bottom line, and may be finally helping the bottom line, but that is less clear.

In the second quarter, Dell’s commercial PC business was flat and its consumer PC business (which is a relatively small part of that PC business) fell by 22.2 percent, causing the overall PC business to drop by 4.1 percent to $12.41 billion. Operating income was really whacked in Q2 for the Client Solutions Group, falling 20.8 percent to $767 million.

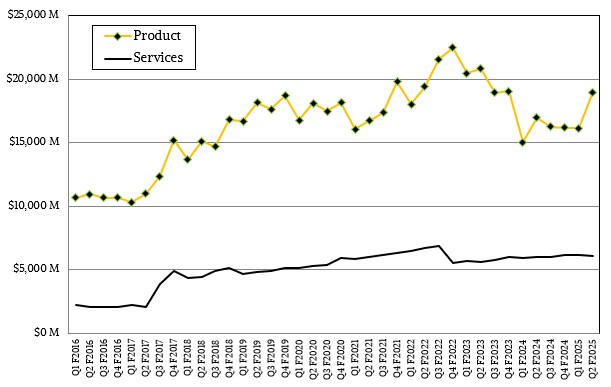

Dell’s overall product revenues, including PCs and datacenter gear, rose by 11.9 percent to $18.95 billion, and services revenues eked out a mere 1.2 percent of growth year on year to $6.07 billion. Product sales were up a healthy 17.5 percent sequentially from fiscal Q1, while services fell by seven-tenths of a point sequentially.

We only care about the client business at Dell inasmuch as it helps pay some of the bills for being an IT supplier and if it is a drag on the business to such an extent that belts have to get tightened.

Overall, Dell’s top-line revenue rose by 9.1 percent to $25.02 billion, operating income rose by 15.2 percent to $1.34 billion, and thanks to cost cutting as well as walking away from deals that do not have enough vig for Big Mike, net income rose by 84.8 percent to $841 million.

Still, that net income represented only 3.4 percent of revenues, compared to the average of 4.7 percent of revenues in the prior three quarters. We think you can blame the PC business, not the Infrastructure Solutions Group that sells servers, storage, and switches into the datacenter.

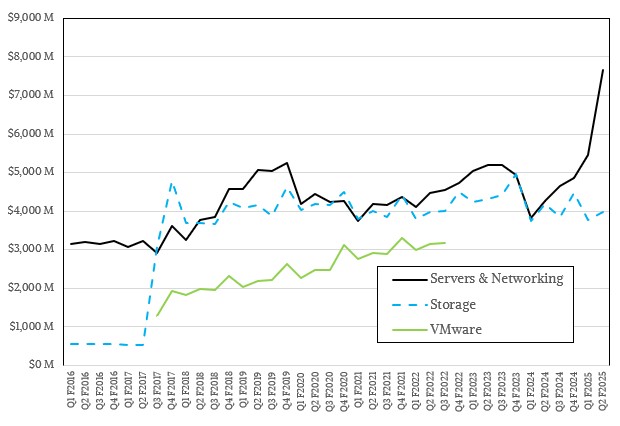

In Q2, Dell’s Infrastructure Solutions Group had $11.65 billion in sales, up 37.6 percent year on year and up 26.2 percent sequentially. A record $7.67 billion in servers and storage were pushed in the quarter, up 79.5 percent compared to Q2 last fiscal year. Storage revenues fell by 5.1 percent to $3.97 billion, and we do not have any reason to believe they will do better in the next two quarters. We also do not believe storage will do much worse, either, as you will see in a moment in the financial model we have built for the remainder of fiscal 2025.

In any event, in Q2, operating income for ISG rose by 22.4 percent, which was at a rate that is significantly lower than the growth in servers and networking and more than fifteen points lower than overall ISG revenue growth. This is not the direction Dell wants operating income numbers to go, of course. But that’s the OEM racket for you. The only thing worse than playing is quitting. . . . And this is exponentially true as we are in the beginning phases of the GenAI Boom.

“We are still in the early innings, and our AI opportunity with tier 2 CSPs, enterprise, and emerging sovereign customers is immense,” Jeff Clarke, Dell’s chief operating officer, explained on the call with Wall Street analysts. “Our view is supported by an AI hardware and services TAM of $174 billion, up from $152 billion, growing at a 22 percent CAGR over the next few years. We are competing in all of the big AI deals and are winning significant deployments at scale.”

“Progress will not always be linear in the early stages, but we are winning in the market with strong feedback from repeat customers while acquiring new customers every quarter. We have the right AI portfolio with more to come, the right services capabilities, and we are optimizing our sales coverage to capture this once-in-a-generation opportunity. With the coming IT hardware recovery cycle and our positioning in AI, I really like our hand.”

Dell had a backlog of $3.8 billion in unfulfilled AI server sales at the end of Q1 F2025, and it fulfilled $3.1 billion in revenues that it booked in Q2 and exited with a $3.8 billion backlog for AI servers. Based on past trends we would have expected a much bigger backload, maybe $4.5 billion, given the demand for AI servers and the tight supplies. But it looks like Dell has reached an equilibrium in that it did $3.1 billion in new deals and sold $3.1 billion in old deals and had the same AI server backlog, of $3.8 billion, amount as Q2 F2025 came to a close.

It is interesting to note that Dell’s AI server business is now about the same size of the VMware portfolio when Michael Dell decided to spin it out as an independent company, which inevitably led to the takeover by Broadcom a few years later.

With these Q2 ISG figures, we can see the interplay of AI server sales against sales of more general purpose machinery, which still dominates the Dell installed base. And based on the figures that Dell gave out for Q3 and full year 2025 revenues, it looks like traditional server sales will stay roughly the same as AI servers stay the same or grow a little bit sequentially.

We have done some estimating for past years based on comments Dell has previously made, and made educated guesses where data was missing.

It is hard to say for sure, even for the top brass at Dell. Over the long haul, we think AI servers will comprise about half of total server revenues worldwide, and there is no reason to believe that, in the fullness of time, this will also be true for Dell’s customers. It may take a few years for enterprises, governments, and Tier 2 service providers to catch up. But if the GenAI Boom is real, then this will happen just like Web infrastructure became something that all organizations on Earth eventually did in some fashion.

The guidance for Dell was pretty wide for the full fiscal 2025 year. Yvonne McGill, Dell’s chief financial officer, said on the call that the company expected revenues of between $95.5 billion and $98.5 billion, with a midpoint of $97 billion, representing 10 percent growth. (It’s actually 9.7 percent, and we are the who in who’s counting.) McGill added that ISG revenues would grow “about 30 percent” for the year, driven by AI servers and “ongoing momentum” in the traditional server business. She added that Dell expected a 1.8 percent hit on gross margin rate for the year due to competition, higher component costs, and a higher mix of AI servers, which leads us to believe that AI servers are still diluting overall profits even if they are technically profitable. (It is hard to imagine anything less profitable than a PC. . . but there you have it.) She added that ISG margin rates would be in the 11 percent to 14 percent historical financial framework that Dell has.

For Q3 of this fiscal 2025 year, Dell expects revenues to be in the range of $24 billion to $25 billion, with the midpoint obviously at $24.5 billion, up 10 percent compared to Q3 of fiscal 2024. ISG is expected to be up “in the low 30s” and PC sales are expected to be flat. ISG operating income is expected to improve.

Given all of these datapoints, here is a table that solves all of those equations in one specific way:

There are many ways to solve this set of simultaneous equations, particularly with a $3 billion error bar across the next two quarters. We are using the midpoints, and we don’t think Dell is guiding a little lower so it can beat but is telling the truth. The midpoints are conservative, and so there is only $1.5 billion of potential additional upside, really.

To constrain out own model, we decided to peg the operating income for ISG in 2025 to match that of ISG in 2024, which is 12.6 percent.

As you can see, to even match the profitability of last year, Q3 has to see a 2.4 points in additional operating margin, and Q4 has to add another 3.7 points on top of that. This seems highly unlikely, but if traditional server margins improve and Dell squeezes storage for more margins while walking away from bad deals, this could happen. We think AI server margins could improve, too, especially with the addition of more support and services now that Dell has some expertise to sell, even if the overall profit rate is lower than ISG as a whole. Hurting the middle line less helps, too.

If we do all that math as shown, then Dell will end 2025 with an AI server business that drove $11.48 billion in sales, up by a factor of 6.34X from the relatively small $1.81 billion in fiscal 2024 and the piddling $118 million we think it did in fiscal 2023.

As you can see in this table, this math also shows the server recession at Dell reversing in the last quarter and, while choppy, still growing and hovering north of $4 billion a quarter going forward and perhaps normalizing to maybe $4.5 billion. In our model, traditional server sales at Dell will rise by 8.4 percent to $17.14 billion.

AI servers will comprise 26.1 percent of ISG server sales for Dell in fiscal 2025 in this model, up from 5.3 percent in fiscal 2024. That is more than halfway to 50 percent right there. (These shares are shown in blue in the bottom right of the chart. Don’t confuse those percents as the growth rates used to the left of the gray separation column.)

We did another thing for perspective for the AI server data. We assume, first of all, that Dell’s AI server figures include any networking it sells in the deal, and we assume the same thing for traditional server sales data, too. But we backed out 20 percent of the revenue in the AI server data, put in an average price of $375,000 for an eight-way GPU server configuration, and then converted that revenue into server units.

If you do this thought experiment, then in fiscal 2024, Dell sold somewhere around 3,900 server nodes with around 31,000 GPUs. That’s it. Roughly equivalent to a single machine that can train GPT-5 or Llama 4 – and not all that fast with people trying to put together machines with 50,000 to 100,000 GPUs to do this job. If the growth for fiscal 2025 pans out as we expect, then Dell will sell around 24,500 eight-way GPU nodes this year, with around 200,000 GPUs.

This is a fraction of many millions of datacenter-class GPUs expected to be sold worldwide over this time.

Letters to the Editor: A love of travel shouldn’t ignore its environmental costs

Cowboys schedule: Is Dallas playing today?

‘A serious disease’: Congress weighs federal gambling crackdown amid growing concerns

Business leaders expect ‘one heck of a fight’ on Texas education

Traffic impacts expected during holiday travel season

Serie A line-ups: Roma vs. Parma

Cutest duo ever: Isha Ambani and daughter Aadiya Shakti steal hearts in matching pink outfits – Times of India

Travel Trends Report 2025: Off-Season Travel

The big winner of the Airbnboom: luxury rentals