Travel

Earnings Beat: Allegiant Travel Company Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

Allegiant Travel Company (NASDAQ:ALGT) shareholders are probably feeling a little disappointed, since its shares fell 5.8% to US$49.83 in the week after its latest second-quarter results. It looks like a credible result overall – although revenues of US$666m were in line with what the analysts predicted, Allegiant Travel surprised by delivering a statutory profit of US$0.75 per share, a notable 15% above expectations. This is an important time for investors, as they can track a company’s performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Allegiant Travel

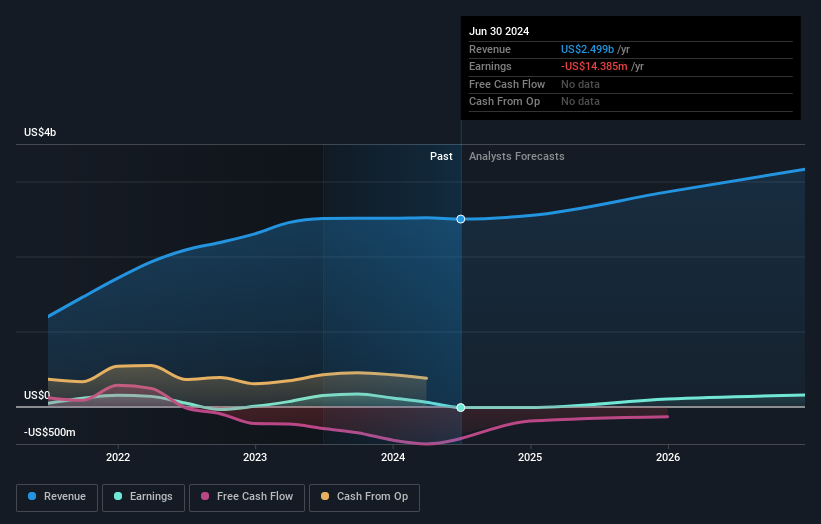

Taking into account the latest results, Allegiant Travel’s nine analysts currently expect revenues in 2024 to be US$2.55b, approximately in line with the last 12 months. Statutory losses are predicted to increase slightly, to US$0.78 per share. Before this earnings report, the analysts had been forecasting revenues of US$2.60b and earnings per share (EPS) of US$2.06 in 2024. While the analysts have made no real change to their revenue estimates, we can see that the consensus is now modelling a loss next year – a clear dip in sentiment compared to the previous outlook of a profit.

As a result, there was no major change to the consensus price target of US$57.70, with the analysts implicitly confirming that the business looks to be performing in line with expectations, despite higher forecast losses. That’s not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Allegiant Travel analyst has a price target of US$87.00 per share, while the most pessimistic values it at US$39.00. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It’s pretty clear that there is an expectation that Allegiant Travel’s revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 3.8% growth on an annualised basis. This is compared to a historical growth rate of 13% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 7.1% annually. Factoring in the forecast slowdown in growth, it seems obvious that Allegiant Travel is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analysts are expecting Allegiant Travel to become unprofitable next year. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. The consensus price target held steady at US$57.70, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company’s earnings is a lot more important than next year. We have forecasts for Allegiant Travel going out to 2026, and you can see them free on our platform here.

You should always think about risks though. Case in point, we’ve spotted 3 warning signs for Allegiant Travel you should be aware of, and 1 of them is potentially serious.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Custom Nuts and Baboon Animation Launch South Asian Office with AZCorp Entertainment

December 4, 2024: Foster mutual trust!")

Cancer Daily Horoscope Today (June 21 – July 22) December 4, 2024: Foster mutual trust!

TPG explores $1.5 billion-plus sale of gym chain Crunch Fitness, sources say

Christian business leaders lend advice at T.W. Lewis Speaker Series – GCU News

")

UTA Signs Fashion and Costume Designer Jonathan Anderson (EXCLUSIVE)

After 50 years, popular family auto shop business closes

C9 focuses on collegiality, role of women, nuncios, and world crises – Vatican News

Deals on Travel Tuesday

Aries, Daily Horoscope Today, December 4, 2024: Family harmony will prevail – Times of India