Travel

Flight Centre Travel Group Limited (ASX:FLT) Stock’s Been Sliding But Fundamentals Look Decent: Will The Market Correct The Share Price In The Future?

Stock’s Been Sliding But Fundamentals Look Decent: Will The Market Correct The Share Price In The Future?")

Flight Centre Travel Group (ASX:FLT) has had a rough month with its share price down 8.2%. But if you pay close attention, you might find that its key financial indicators look quite decent, which could mean that the stock could potentially rise in the long-term given how markets usually reward more resilient long-term fundamentals. Particularly, we will be paying attention to Flight Centre Travel Group’s ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for Flight Centre Travel Group

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders’ Equity

So, based on the above formula, the ROE for Flight Centre Travel Group is:

13% = AU$154m ÷ AU$1.2b (Based on the trailing twelve months to December 2023).

The ‘return’ is the yearly profit. One way to conceptualize this is that for each A$1 of shareholders’ capital it has, the company made A$0.13 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company’s future earnings. We now need to evaluate how much profit the company reinvests or “retains” for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don’t necessarily bear these characteristics.

Flight Centre Travel Group’s Earnings Growth And 13% ROE

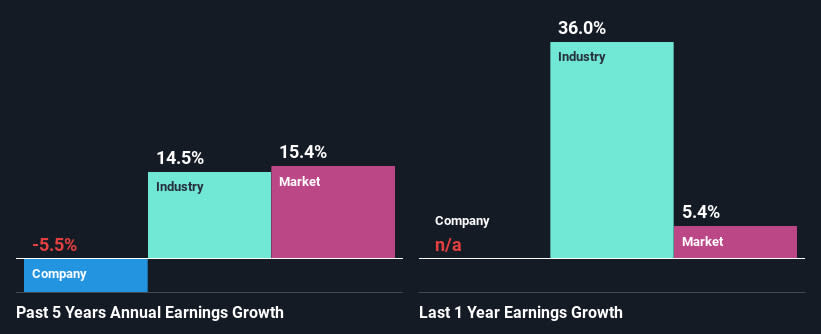

At first glance, Flight Centre Travel Group seems to have a decent ROE. Further, the company’s ROE is similar to the industry average of 12%. However, while Flight Centre Travel Group has a pretty respectable ROE, its five year net income decline rate was 5.5% . So, there might be some other aspects that could explain this. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for instance.

So, as a next step, we compared Flight Centre Travel Group’s performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 15% over the last few years.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company’s expected earnings growth (or decline). Doing so will help them establish if the stock’s future looks promising or ominous. What is FLT worth today? The intrinsic value infographic in our free research report helps visualize whether FLT is currently mispriced by the market.

Is Flight Centre Travel Group Using Its Retained Earnings Effectively?

Looking at its three-year median payout ratio of 48% (or a retention ratio of 52%) which is pretty normal, Flight Centre Travel Group’s declining earnings is rather baffling as one would expect to see a fair bit of growth when a company is retaining a good portion of its profits. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

In addition, Flight Centre Travel Group has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Based on the latest analysts’ estimates, we found that the company’s future payout ratio over the next three years is expected to hold steady at 53%. Still, forecasts suggest that Flight Centre Travel Group’s future ROE will rise to 22% even though the the company’s payout ratio is not expected to change by much.

Conclusion

Overall, we feel that Flight Centre Travel Group certainly does have some positive factors to consider. However, given the high ROE and high profit retention, we would expect the company to be delivering strong earnings growth, but that isn’t the case here. This suggests that there might be some external threat to the business, that’s hampering its growth. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company’s earnings growth rate. To know more about the company’s future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Amazon has PS5 consoles on sale up to $126 off on Black Friday — but only for a limited time

KSA Fines BetOnline Owner for Illegal Gambling in the Netherlands

World Athletics Ultimate Championship events announced, including mixed 4x100m relay

Five Tips To Maximize Profits On Small Business Saturday And Beyond

Apple reportedly developing conversational Siri using LLMs

Nordstrom Black Friday: Store hours, top deals, everything to know

‘Invisible to the outside world’: IT business proposes hidden Columbia County data center

Billionaire Adani’s Conglomerate Faces Scrutiny And Setbacks Around The World Amid U.S. Indictment

What to expect for Thanksgiving travel at Columbus airport this year