Bussiness

Horrible Small Business Earnings

Hiroshi Watanabe

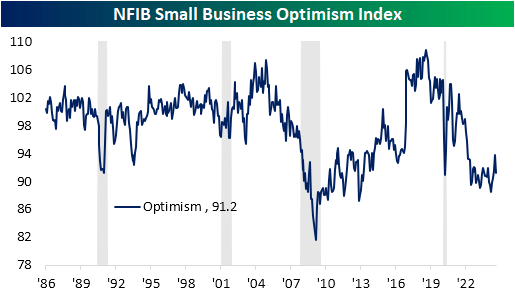

This morning’s NFIB Small Business Optimism Index showed disappointing results. The index was expected to show small businesses had less optimism with the index forecasted to fall 0.1 points month over month down to 93.6.

Instead, the decline was much more dramatic as it fell down to 91.2; erasing all of the summer gains. One factor likely at play that we have noted in the past is political sensitivities.

Historically speaking, NFIB data has tended to hold a positive bias during Republican administrations and vice versa. Put differently, optimism rises when Republicans are in power or are expected to be voted in, and optimism falls when Democrats are in power or are expected to win an election.

In reaction to last month’s report, we discussed how the recent surge in optimism earlier this summer was concurrent with the rising odds of former President Trump winning back the presidency.

This latest data, on the other hand, would capture that the Presidential race is looking tighter than it did previously, and optimism seems to have moved lower in turn.

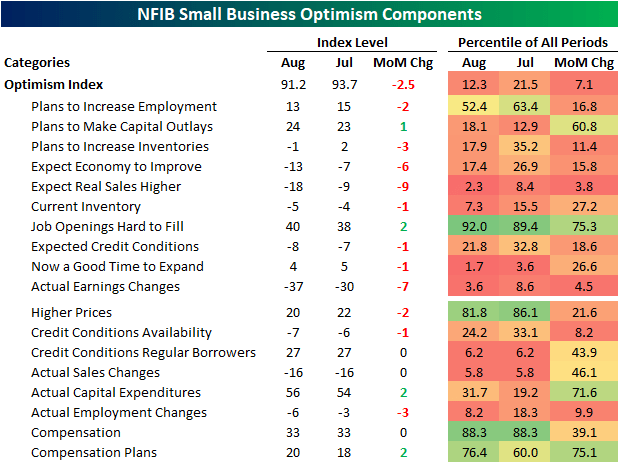

Looking under the hood of the report, there wasn’t much to like. Of the inputs to the Optimism Index, only two rose month over month: Plans to Make Capital Outlays and Job Openings as Hard to Fill. The latter of those is by far the strongest category of the report with the August reading in the 92nd percentile of all months.

Outside of that, there are four inputs to the optimism index and another three non-input categories that now rank in the bottom decile of readings. Some of those like Actual Earnings Changes and Expectations for Higher Real Sales also fell significantly month over month with bottom decile monthly moves.

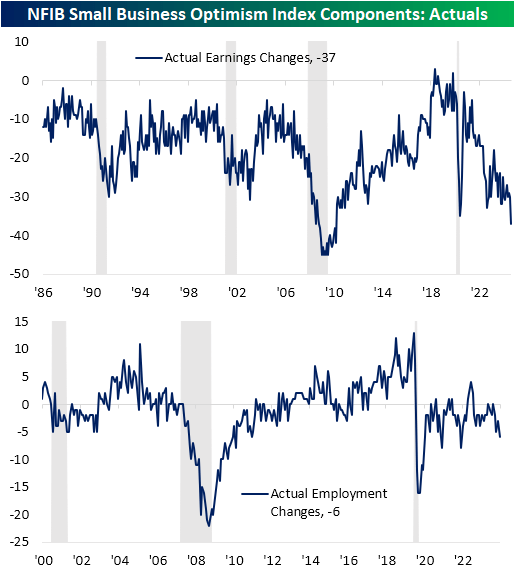

As noted above, one of the weaker inputs to optimism was actual earnings changes and other “actual” categories are similarly weak. In August, that index fell 7 points month over month. That is the largest decline in a single month since last October when it fell 8 points.

More impressively, that drop results in the index falling below the spring 2020 lows for the worst reading since March 2010. Among other categories for observed (rather than expected) conditions, employment change reached a new near term low of -6.

That is the weakest reading in this index in two years. As we showed in the Morning Lineup, combined with other labor market categories, the report is consistent with a further weakening labor market.

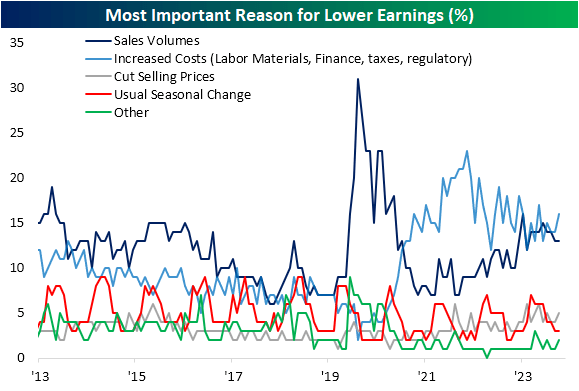

Circling back on the weak change to earnings, the report details a handful of reasons that small businesses are reporting lower earnings. As shown below, the most common response in August was increased costs; up 2 percentage points to 16%. The next most common reason was sales volumes, which was unchanged sequentially at 13%.

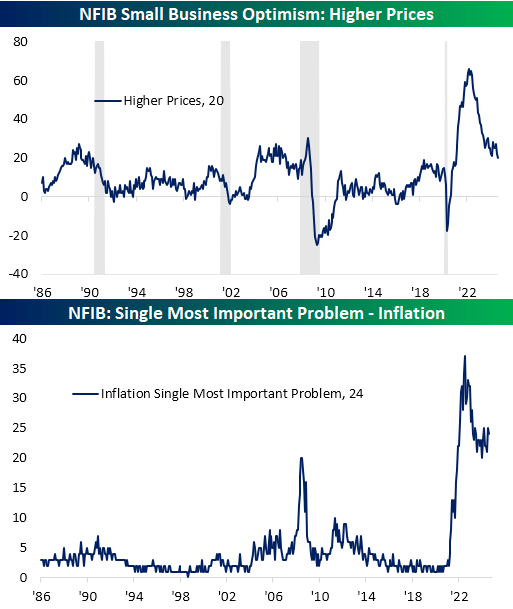

While those responses would indicate that an uptick in inflation has been hurting the bottom line of small businesses, the report’s inflation gauge was somewhat contradictory. There continues to be more companies reporting that prices are higher versus lower than they were three months ago.

However, that higher prices index has been improving dramatically. The index dropped to a new low of 20 in August, which is the lowest level since January 2021.

While that is also still elevated ranking in the 81st percentile of all months on record, that is well below the peak from two and a half years ago and is consistent with decelerating inflation. Additionally, the share of businesses reporting inflation as their biggest problem ticked down modestly to 24% from 25% and is well below the highs near 35%.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Brown states Kings fans ‘deserve better’ after loss to Pacers

Gift wrapping and last minute shopping at the West Park Mall

‘Smooth sailing so far,’ holiday travel rush in full swing at PHL

High school sports scores, schedule for Dec. 22, 2024 | Trib HSSN

College basketball rankings: Auburn, Tennessee on top; Michigan State climbing

Katrina Kaif walks hand in hand with Vicky Kaushal in stylish winter outfit. Loved her trench coat? Here’s how to get it

Numerology Horoscope Today: Predictions for December 23, 2024

Valeri Nichushkin with a Goal vs. Seattle Kraken

US fitness influencer dies at 43, months after being shot during LA robbery