In 2021, the cryptocurrency market regained the public’s attention

as the value of one Bitcoin broke through its previous all-time high of nearly

$20,000 to reach a price of almost $70,000.

However, in 2022, the market suffered numerous high-profile

failures, including the crash in value of stablecoin provider Terra’s UST and the collapse of crypto exchange FTX. By

2024, the fallout from those events and others, and subsequent bear market (in

which many cryptocurrencies fell 90% from their heights), meant that crypto had

once again faded from the average person’s consciousness.

Although sentiment turned positive as Bitcoin rallied and again

crossed $70,000 in March 2024, driven by the approval of Bitcoin ETFs (which allow investment in futures contracts rather than

cryptocurrency itself), concern regarding the market still lingers for many.

This concern has been heightened by pending governmental regulations designed

to limit cryptocurrency growth, such as the Security and Exchange Commission’s

litigation efforts classifying many cryptocurrencies as securities.

The regulator has filed lawsuits against 31 crypto firms it accused of violating U.S. securities

law. Although the SEC ended one of its investigations in June, given the crypto sector’s

tumultuous history it is unsurprising that many in the travel industry have

dismissed cryptocurrency as a passing fad, as they did after the comparable

2017 crypto and blockchain hype bubble popped.

Subscribe to our newsletter below

However, flying under the typical travel industry radar is the fact

that the central banks of many nations have begun issuing digital currencies of

their own. These central bank digital currencies (CBDCs) have characteristics

similar to cryptocurrencies, but with one critical difference: As opposed to

the decentralized nature of many cryptocurrencies, with Bitcoin being the prime

example, CBDCs are fully centralized and have been created, promoted and

controlled by existing central banks. For more on centralization versus

decentralization, see The Decentralized Computing

Future (2021).

The purpose of a CBDC is to act as a digital version of a country’s

currency. As few travel suppliers and retailers currently accept digital

currency today, the introduction of state-sponsored digital currency adds a new

wrinkle to the types of payments that would need to be accepted.

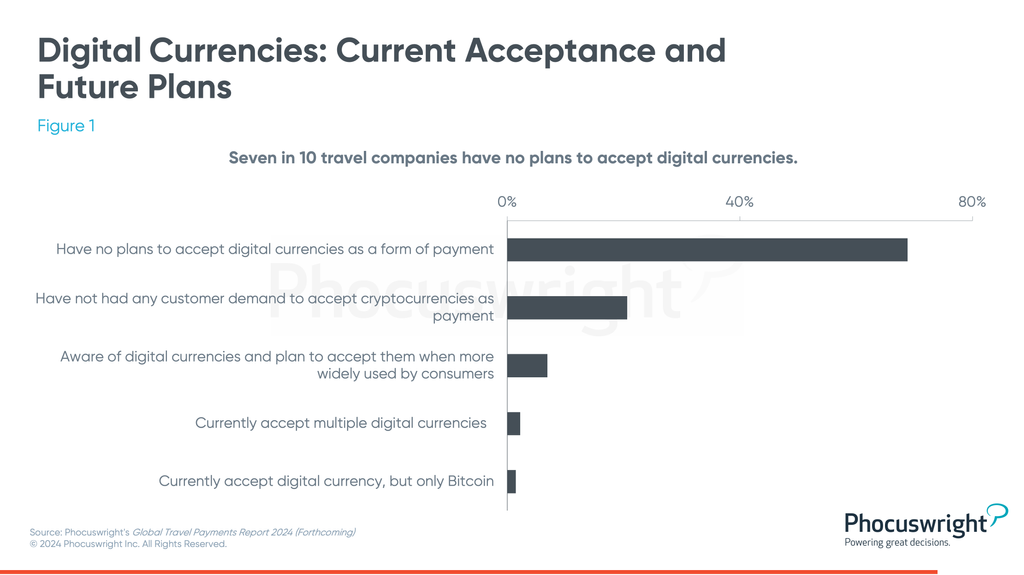

Phocuswright’s

forthcoming Global Travel Payments Report 2024 illustrates the lag in

acceptance of digital currencies, with seven in 10 travel companies having no

plans to accept them.

CBDC’s impact on the travel industry

To succeed, CBDCs need to fit within the current payment

infrastructure. A central bank may issue this digital money to financial

institutions for distribution, or even directly to a consumer’s digital wallet.

The consumer would pay at checkout much the same way they do today

with a phone. The only caveat is that the wallet needed for this transaction

must be a software wallet that stores value.

For a description of wallet types, see Who Owns the Customer? How About

the Customers Themselves! The

article also addresses the need for software wallets to hold self-sovereign

identity (SSI) profiles. If CBDCs proliferate, these may act as a means for

greater distribution of software wallets as well.

To prepare for the emergence of CBDCs, travel companies

should:

- Evaluate global markets, recognize those that are advancing their

CBDC timetable and analyze its impact on travel payment strategies. - Join working groups such as the European Central Bank’s “Call for candidates to

participate in the digital euro scheme infrastructure-related requirements

workstream.” - Assign a team or individual to become educated on CBDCs, track

their progress and contribute to a strategy for CBDC acceptance based on

overall market acceptance.

While consumer adoption of digital currencies thus far has been

slow, full rollouts of CBDCs in the coming years means most consumers will have

access to digital currency as a form of payment.

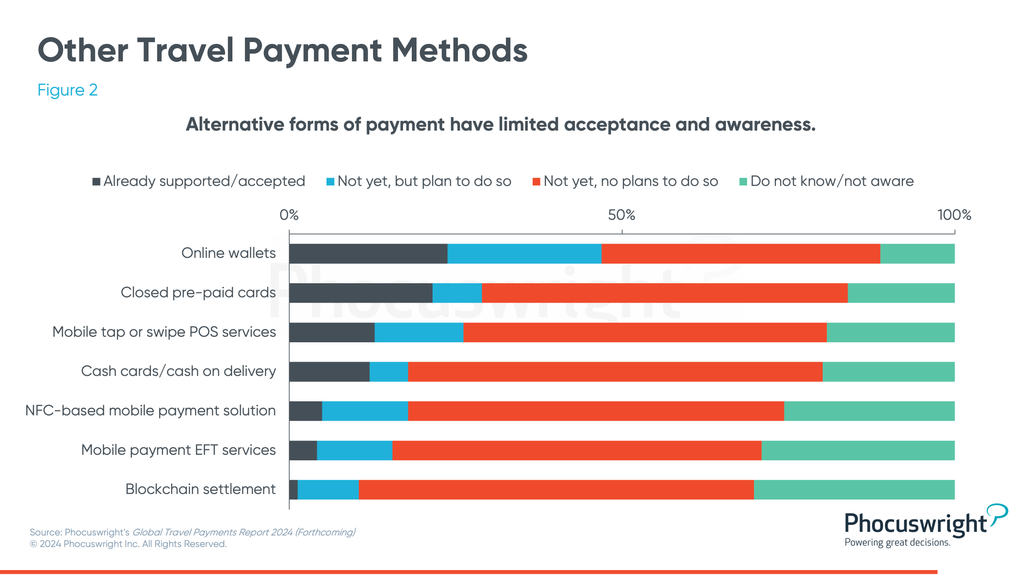

The travel industry currently struggles with alternative forms of

payment, and therefore the shift to full digital currencies, even those

provided by the government, will require broad industry collaboration. In

Phocuswright’s forthcoming Global Travel Payments Report 2024, travel companies

of all sizes and in various geographies exhibit a resistance to the adoption alternative

forms of payment (AFPs), though global acceptance is growing in other

industries.

The dust has not settled on the CBDC issue, but clearly multiple

governments are pushing ahead with their CBDC efforts and preparations need to

be made.

{kind=link}