Entertainment

Live Nation Entertainment Stock Up 16% in a Year: Should You Buy?

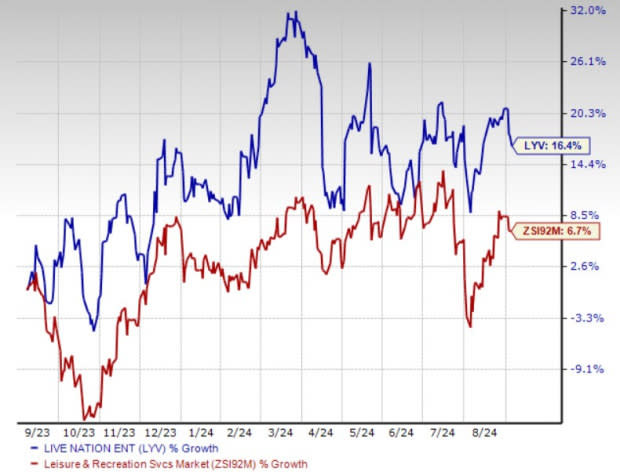

Shares of Live Nation Entertainment, Inc. LYV have gained 16.4% in the past year, outperforming the industry’s growth of 6.7%.

As of Thursday, the stock closed at $94.20, below its 52-week high of $107.24 but above the low of $76.48. The company is benefiting from robust global fan demand for live events, resulting in increased ticket sales.

Stock Price Performance

Image Source: Zacks Investment Research

Factors Favoring LYV

The company is concentrating on enhancing Venue Nation’s fan experience and hospitality services. Venue Nation is projected to welcome more than 60 million fans this year, marking a 10% increase from the previous year. Average spending per fan at Live Nation amphitheaters is aiding the company.

Robust demand continues to drive Live Nation Entertainment’s performance. For concerts, the company stated that it has already sold more than 118 million tickets year to date, up from the same period in 2023, with double-digit increases for arena, amphitheater and theater and club shows. In second-quarter 2024, the Concerts segment’s revenues increased 8% year over year to $4.99 billion.

The company plans to open 14 major venues worldwide in 2024 and 2025 to boost its market presence. To support this expansion, capital expenditures for 2024 are anticipated to reach $650 million. These initiatives aim to drive substantial revenue growth and reinforce the company’s market position.

The company is very optimistic about its growth prospects for 2024. LVY expects to see improved margins in its Concert segment, driven by revenues from beer sales, parking and other sources, along with higher ticket prices. Live Nation Entertainment is counting on several of its artists, including Drake, to embark on multi-year tours across the United. States and Europe, which is expected to boost the company’s performance. Concerts are projected to be a key growth driver this year and the company anticipates that margins will approach 2019 levels.

Factors That May Hinder LYV Stock Growth

Although the stock has gained 4.6% in the past month, it has underperformed its industry’s growth of 9.5%.

The company witnesses cost hikes due to increased labor-hiring costs, artist activation costs and other operational expenses. Also, it has been witnessing a rise in venue costs and service fees. In second-quarter 2024, total direct operating expenses were $4.41 billion, up from $4.16 billion in the prior-year quarter. The company is cautious of cost overruns related to the development and expansion of live music venues. An increase in costs is likely to affect its bottom line.

The company’s ticketing business continues to face competition from a multitude of national, regional and local primary ticketing service providers as they continually strive to attract and retain clients. Additionally, the emergence of self-ticketing systems offered by various companies poses challenges, with clients increasingly opting for self-ticketing methods through system integration or the acquisition of primary ticket service providers. This competition is further compounded by heightened sales through venue box offices and season and subscription sales.

LYV Trading at a Premium

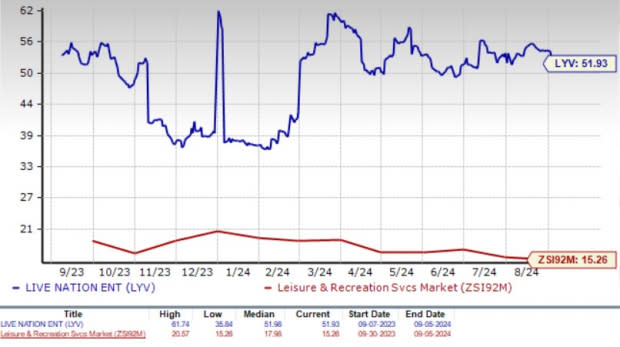

The company is currently valued at a premium compared with the industry and the S&P 500 on a forward 12-month P/E basis. LYV’s forward 12-month price-to-earnings ratio stands at 51.93, significantly higher than the industry’s ratio of 15.26 and the S&P 500’s ratio of 21.13. The company is also trading currently at a premium compared to consumer discretionary stocks like Caesars Entertainment, Inc. CZR, Six Flags Entertainment Corporation FUN and Travel + Leisure Co. TNL.

P/E Ratio (F12M)

Image Source: Zacks Investment Research

Conclusion

Live Nation Entertainment is benefiting from robust global demand for live events, leading to increased ticket sales and improved revenues in the Concerts segment. Its strategic focus on enhancing fan experiences, expanding Venue Nation and opening new venues worldwide positions it well for growth. However, LYV faces challenges that may temper its near-term upside potential. Rising costs, including labor, artist activation and venue expenses, are pressuring its margins.

Given these dynamics, it would be prudent for current investors to hold onto their shares, capitalizing on the company’s solid market position and growth initiatives. Still, new investors might want to wait for a more favorable entry point, considering the potential risks and the stock’s current valuation. LYV currently has a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Live Nation Entertainment, Inc. (LYV) : Free Stock Analysis Report

Six Flags Entertainment Corporation (FUN) : Free Stock Analysis Report

Caesars Entertainment, Inc. (CZR) : Free Stock Analysis Report

Travel + Leisure Co. (TNL) : Free Stock Analysis Report

SNF open thread: Buccaneers-Cowboys gambling lines and picks for tonight’s game

Fantasy Football Waiver Wire: Early pickups for Week 17

Holiday shopping in San Ysidro draws people from both sides of the border

Be prepared for record-breaking holiday travel, AAA says

Boston shoppers brave bitter cold to get last-minute gifts on Newbury Street

‘CES is no longer just about consumer tech’

Thunder, Alex Caruso reportedly agree to 4-year, $81 million extension

")

The Crazy, Confused World Of Used Cybertruck Pricing (Update)

‘It’s fun:’ Fromberg woman turning candle making hobby into business